Choosing a Small Business Retirement Plan

As a small business owner, you’ve reached a certain level of success and built a comfortable future for your family. Depending on the size of your company, you’ve also created jobs, so your employees can provide for their families. But what’s the next step?

Presented by Gerard Longo, AIFA®, CPFA®:

Establishing an employer-sponsored retirement plan for your small business will help ensure that you and your employees have a steady stream of income—even after you retire. There are many types of retirement plans available to companies, but a select few are most beneficial to small business owners. SEP IRAs, SIMPLE IRAs, and safe harbor 401(k)s are the most commonly used plan types because of their simplicity, affordability, and minimal administrative requirements.

An Overview of Each Retirement Plan Type

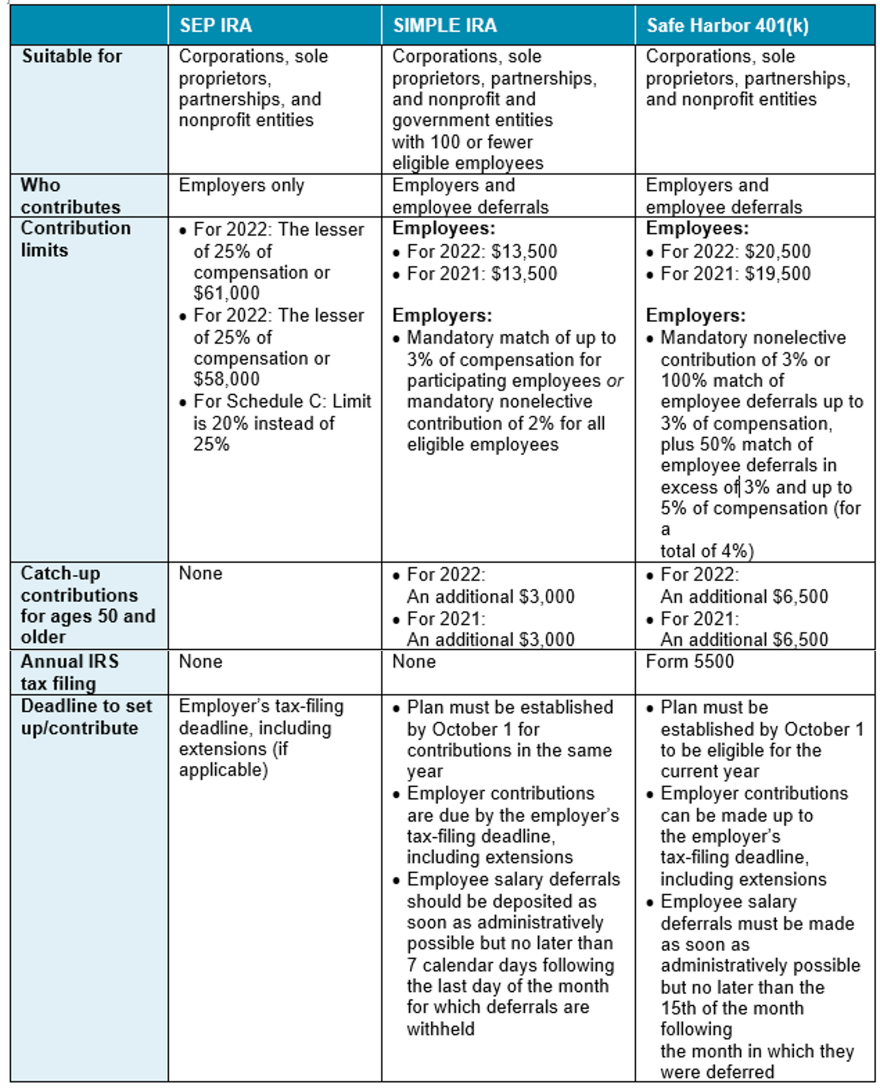

To help you determine the best retirement plan for your business, the information below highlights the major benefits of each plan type, as well as important considerations to keep in mind.

SEP IRA

Benefits

- The SEP-IRA retirement plan is easy to set up and administer.

- Annual compliance testing and IRS filings are not required.

- Contributions are tax deductible.

- Employer contributions can vary each year, and they do not have to be made every year.

- Example: An employer can contribute 4 percent one year, 0 percent the next year, and 2 percent the year after that.

- Employers can exclude certain employees, such as anyone younger than 21, those who have not been employed for at least three of the past five years, or those who have earned less than $650 in either the current or prior year.

Important Considerations

- This plan is employer funded only.

- The same contribution percentage must be used for all eligible employees, including you as the employer.

- Loans are not allowed.

SIMPLE IRA

Benefits

- A Simple IRA retirement plan is easy to set up and administer.

- Annual compliance testing and IRS filings are not required.

- Employer contributions are tax deductible.

- Employees can contribute to this plan.

- Employers can exclude employees who have not received at least $5,000 in compensation during any two preceding calendar years (do not have to be consecutive years) and who are not expected to earn at least $5,000 in the current year.

Important Considerations

- Employer contributions are mandatory. Employers must make either a nonelective 2 percent contribution to all eligible employees regardless of participation or match 100 percent of employee deferrals up to 3 percent of compensation.

- SIMPLE IRAs have a unique two-year rule associated with their distributions and rollovers. They cannot be rolled over to any other retirement account (except another SIMPLE IRA) within the two-year period beginning on the first date of participation in the plan. In addition, IRA owners younger than 59½ who distribute within the two-year time frame (in which a premature distribution exception does not apply) will be fined a 25 percent premature penalty instead of the normal 10 percent penalty.

- Loans are not allowed.

Safe Harbor 401(k)

Benefits

- The Safe Harbor 401(k) retirement plan has the same features as a traditional 401(k) without the annual nondiscrimination testing.

- Employer contributions are tax deductible.

- Employees are allowed to contribute.

- Profit-sharing contributions from the employer are allowed.

- Loans are allowed.

Important Considerations

- Employer contributions are mandatory. For a 401(k) to be a safe harbor plan, employers must do one of the following:

- Make a nonelective 3 percent contribution to all employees regardless of participation.

- Match 100 percent of employee deferrals up to 3 percent of compensation, plus 50 percent of employee deferrals in excess of 3 percent and up to 5 percent of compensation (for a total of 4 percent).

- Although nondiscrimination testing is not required, Form 5500 must still be filed annually.

- Distributions from this plan require a triggering event.

{kind=link}

Which Retirement Plan Should You Choose?

With so many choices available, it can be difficult to find the right fit. You might start by asking, “What’s most important to me in a retirement plan?” Here are a few examples:

- If low cost and minimal maintenance are priorities for your business, a SEP or SIMPLE IRA would be an appropriate fit.

- If you have highly compensated employees and want to give them the opportunity to maximize their retirement savings, a safe harbor 401(k) would allow for that, as long as you are willing to make the employer match.

- If you are a sole proprietor with no employees and want to maximize your own retirement savings, a SEP IRA could be your best option.

By understanding what each plan has to offer (and what it doesn’t), you’ll be well prepared to make the best choice for your retirement, as well as the retirement of your employees.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

Learn more about IRA SEPP Distributions.

###

Gerard Longo is a financial advisor located at Global Wealth Advisors 2400 Ansys Drive, Suite 102, Canonsburg, PA 15317. He offers advisory services through Commonwealth Financial Network®, Member FINRA / SIPC, a Registered Investment Adviser. Financial planning services offered through Global Wealth Advisors, LLC are separate and unrelated to Commonwealth. Gerard can be reached at (412) 914-8292 or at info@gwadvisors.net.

© 2022 Commonwealth Financial Network