Quarter End Report

Presented by Keith Sprauer, MBA, MS

Stocks Rally in September

Stocks continued their recent rally in September, with all three major U.S. indices up for the month and quarter. The S&P 500 gained 2.14 percent in September and 5.89 percent for the quarter, while the Dow Jones Industrial Average (DJIA) was up 1.96 percent during the month and 8.72 percent for the quarter. Both the S&P 500 and DJIA hit new record highs in September before falling back modestly to end the month. The technology-heavy Nasdaq Composite gained 2.76 percent for the month and quarter as technology stocks experienced heightened turbulence over the summer compared to the broader market.

These positive results were supported by improving fundamentals. Per Bloomberg Intelligence, the average earnings growth rate for the S&P 500 in the second quarter was nearly 14 percent. This is well above analyst estimates at the start of earnings season for a more modest 8.3 percent increase. Because fundamentals ultimately drive long-term market performance, this was an encouraging development for investors as it showcased the continued health of American businesses.

Technical factors were supportive as well for the month and quarter. All three major indices spent the entire month well above their respective 200-day moving averages. (The 200-day moving average is a widely tracked technical signal, as prolonged breaks above or below this level can indicate shifting investor sentiment for an index.) All three of the major U.S. indices have spent the entire year above their respective trendlines, indicating continued investor support for U.S. stocks.

The story was similar internationally for the month and quarter. The MSCI EAFE Index gained 0.92 percent in September, capping off a 7.26 percent gain for the quarter. The MSCI Emerging Markets Index surged 6.72 percent in September, which contributed to an 8.88 percent gain for the quarter. The announcement of major stimulus policies in China toward the end of the month led to the outperformance for emerging markets in September.

Technical factors were supportive for international stocks during the month. Both indices spent the entire month above trend. This was especially encouraging for the emerging market index, which had previously briefly dipped below its 200-day moving average in early August.

Strong Quarter for Bonds

September was another positive month for bonds, capping off a strong quarter for fixed income investors. Falling interest rates over the month and quarter helped support bond returns throughout the summer. The 10-year Treasury yield fell from 4.48 percent at the start of July to 3.81 percent by the end of September. Short-term rates fell notably as well during the quarter due to heightened expectations for Fed rate cuts. The Bloomberg Aggregate Bond Index gained 1.34 percent during the month and an impressive 5.20 percent in the third quarter.

High-yield fixed income, which is typically less driven by interest rate movements, also had a strong month and quarter. The Bloomberg US Corporate High Yield Index gained 1.62 percent in September and 5.28 percent for the quarter. High-yield credit spreads compressed from 3.21 percent at the start of the quarter to 3.03 percent at quarter-end. Tighter credit spreads indicate increased investor appetite for high-yield investments.

Federal Reserve Cuts Interest Rates

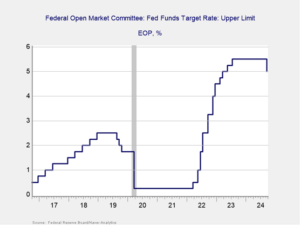

The Fed cut the upper target of the federal funds rate by 50 basis points at the conclusion of its September meeting. This brought the upper limit from 5.50 percent down to 5.0 percent. As you can see in Figure 1, this marked the first interest rate cut in more than four years and indicates that the Fed is shifting away from the restrictive monetary policy that we’ve recently experienced in favor of more supportive policy ahead.

Figure 1: Federal Open Market Committee Federal Funds Target Rate Upper Limit, October 2016–Present

Source: Federal Reserve Board/Haver Analytics, September 18, 2024.

The 50-basis-point cut was larger than most economists had anticipated; however, it was in-line with market pricing heading into the meeting. Fed chair Jerome Powell indicated in his post-meeting press conference that the Fed remains committed to its dual mandate of promoting stable prices and maximum employment. Given the improvements that we’ve seen on the inflation front over the past two years, central bankers decided that the time was right to shift toward a more accommodative policy given recent signs of potential weakness in the labor market.

Markets rallied following the Fed’s announcement, as lower interest rates can help support valuations and fundamentals. Looking forward, futures markets have priced in expectations for additional rate cuts through the end of this year and into 2025. Although the Fed raised rates throughout 2022 and 2023 and kept them high in 2024 to combat inflation, looking ahead, this headwind is set to shift into a tailwind for markets and the economy.

The Takeaway

- The Fed cut interest rates by 50 basis points at its September meeting.

- Further rate cuts are expected through the end of this year and into 2025.

Healthy Economic Backdrop

While interest rates were the primary story in September, economic updates released during the month were also encouraging. Hiring rebounded as a solid 142,000 jobs were added in August, up from a downwardly revised 89,000 in July. The unemployment rate also fell from 4.3 percent in July back down to 4.2 percent in August. While the pace of hiring has slowed since earlier in the year, slower growth is still growth, and job creation at these levels is a sign of continued economic expansion, especially following years of above-average job growth.

One of the benefits from the recent years of strong hiring that we’ve seen is that consumers remain willing and able to spend. That remained the case in August as retail sales growth came in above economist estimates and personal spending grew for the 17th consecutive month. Consumer spending is the major driver of U.S. economic activity and has remained impressively resilient over the course of the year.

Business activity was also healthy during the month, as durable goods orders came in above estimates. Industrial and manufacturing production also rebounded well past expectations following weather-driven declines earlier in the summer.

Finally, we even saw improvements on the inflation front, with year-over-year CPI growth falling to 2.5 percent in August, down from 2.9 percent in July. This marks a more than three-year low and highlights the improvements that we’ve seen over the past two years when it comes to inflation. While there is still real work to be done to get inflation back to the Fed’s 2 percent target, the continued improvement in August was certainly welcome.

The Takeaway

- The economic data releases in September showed signs of continued economic growth.

- Hiring rebounded in August and consumer spending remained robust.

- Inflation continued to fall, highlighting the improvements that we’ve seen over the past two years.

Real Risks Remain

While the fundamentals and economic backdrop remain supportive for investors, there are real risks that markets face, which should be mentioned. The primary risk domestically is a further economic slowdown in the months ahead. The labor market will be key to monitor here, as any additional weakness could be a sign of potential slowing economic growth. Additionally, political uncertainty is expected to continue to rise as we approach the November elections.

Foreign risks remain as well, as shown by the ongoing conflicts in Ukraine and the Middle East as well as the slowdown in China. These sources of potential uncertainty could escalate and lead to additional regional and global market volatility. And, of course, there are also the unknown risks that could negatively impact markets at any time.

The Takeaway

- The health of the labor market and rising political uncertainty are risks worth monitoring.

- International and unknown risks should be acknowledged as well.

Cautious Optimism Warranted

Despite the real risks that markets face, overall, we remain in a relatively good place as we finish out the third quarter and head into the end of the year. Market fundamentals remain sound and the economic backdrop is expected to remain broadly supportive through the end of the year. Additionally, the headwind from high interest rates that we’ve experienced over the past two years is set to transition to a tailwind in the months ahead.

While there are certainly sources of potential uncertainty that investors should be aware of, the outlook remains cautiously optimistic as further market appreciation and economic growth remains the most likely path forward. Of course, we may face short-term setbacks along the way and, therefore, a well-diversified portfolio that matches investor goals and timelines remains the best path forward for most. As always, if concerns remain, you should speak to your financial advisor to review your financial plans.

Disclosure: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent.

###

Check out our current weekly update.

Refer back to this year’s outlook to see what was predicted and where we actually are this quarter.

Keith Sprauer, MBA, MS is a chief investment officer located at Global Wealth Advisors 4400 State Highway 121, Suite 200, Lewisville, TX 75056. Securities offered through Commonwealth Financial Network®, member FINRA / SIPC.

Authored by Brad McMillan, CFA®, managing principal, chief investment officer, and Sam Millette, director, fixed income, at Commonwealth Financial Network®.

© 2024 Commonwealth Financial Network®